{kind=link}

From Claims to Fairytales: How to Write for Different Audiences | Chantal Roberts

The Leveraging Thought Leadership podcast is created by Peter Winick and Bill Sherman and produced by Thought Leadership Leverage.

![]()

![]()

An Author’s Journey Writing Two Books for Two Very Different Audiences

In this episode, Chantal Roberts shares with us how she went about writing a highly technical book for a technical audience, and a general book on the same topic for a more common audience.

How do you turn technical expertise into a story that captures everyone’s attention?

Today, host Bill Sherman sits down with Chantal Roberts, an insurance expert and professor at The Borough of Manhattan Community College in New York., to discuss her unique journey as an author of two distinct books. One caters to insurance professionals, and the other takes a creative approach to educate the general public.

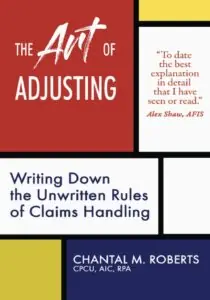

Chantal’s first book, The Art of Adjusting, targets mid-career insurance adjusters, offering them insights into the unwritten rules of claims handling. With remote work reducing informal knowledge-sharing, she aimed to bridge that gap. This book also strengthened her credentials as an expert witness in insurance litigation.

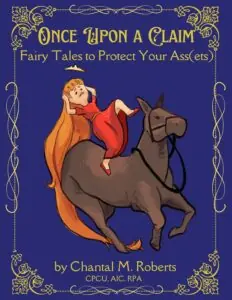

Her second book, Once Upon a Claim: Fairytales to Protect Your Assets, was a complete pivot. Inspired by her experience teaching, Chantal decided to use fairy tales like Rapunzel and Goldilocks to explain complex insurance concepts to consumers. The goal? To help people understand the claims process better and avoid feeling blindsided.

Chantal shares how her passion led her to write in ways that even surprised her. She also discusses her grassroots marketing efforts, sending postcards to agents as a way to spread the word about her second book—ensuring it doesn’t get lost in the spam folder. If you’re wondering how to write for different audiences without losing your authentic voice, Chantal’s journey is full of insights.

Three Key Takeaways:

Tailor your message to the audience: Chantal’s books serve two very different audiences—insurance professionals and general consumers—requiring her to adjust both her tone and content to suit their needs.

Passion drives engagement: If you don’t love what you’re writing, neither will your readers. Chantal’s pivot from a technical rewrite to storytelling with fairy tales made her second book more engaging and enjoyable for everyone.

Creative marketing matters: Chantal’s approach to promoting Once Upon a Claim through physical postcards demonstrates the power of thinking outside the box to avoid digital clutter and create a personal touch.

Chantal uses a different approach to finding her audience, but are you still using mass market techniques with your niche audience? If so, this article by Thought Leadership Leverage founder and CEO Peter Winick might be helpful.

Transcript

Bill Sherman It’s hard to write a one size fits all readers book. You can either create a book that’s too simple for people familiar with your topic, or you can overwhelm a potentially larger general audience. Today, I speak with Shawn Tal Roberts, an insurance expert, professor at Borough of Manhattan Community College and the author of two books around the topic of insurance. Her first book was for Adjusters, those who were a few years into their career and needed to learn the nuance. And her second book is for a Popular audience. Today, we’ll explore how to calibrate a book to your audience’s needs, and we’ll explore how the journey of publishing for different purposes and different audiences leads to different impact. I’m Bill Sherman. You’re listening to Leveraging Thought Leadership. Ready? Let’s begin. Welcome to the show, Chantal.

Chantal Roberts Thank you. Thanks for having me. So.

Bill Sherman I want to explore the process of writing books for you. And you’ve written two very different books for very different purposes and audiences. One much more technical and credential building. The other for general popular audience. Right. So let’s start with the first book. What was that topic of that first book and why did you write it?

Chantal Roberts The topic of the first book was for insurance adjusters in their mid-career, you know, five, ten, 15 years. And the purpose of that book, The Art of Adjusting, was to actually do what the subtitle says is writing down some of these unwritten rules that adjusters have and try to help make their lives easier since people are being promoted. Or maybe you don’t have time to be trained or what have you. That is the purpose of the art of adjusting.

Bill Sherman And so that book is a combination of you teach in this topic. You also practiced in this area beforehand. So you came up with some expertise rather than drawing out of the great grand fishbowl of book topics and picking insurance and just it. Right?

Chantal Roberts Yeah, absolutely. Yes. I always enjoyed teaching even when I was a claims manager at a third party administrator, we handled claims for some syndicates at Lloyd’s of London. And I always enjoyed teaching the adjusters. And there are a lot of little tidbits that help adjusters handle their claims better because adjusters get yelled at a lot, obviously because people are not happy with us. They think that we just deny their claims or we’re not paying them enough. So there are techniques that an adjuster can use that a lot of times people may not know, especially now that the majority of us are remote. They don’t hear their manager talking or they don’t hear their coworkers talking because we’re no longer in like a little tube for lack of a better term.

Bill Sherman Well, and you mention Lloyd’s of London, which goes back centuries and the history of insurance. And there is if you think about insurance policies and even the process of claims adjustment, almost a. Apprentice relationship that started out early on and anecdotal relation is stories of yeah, there was that one time that we had the ship that sank, but this condition therefore we did that. So there’s a lot of experiential knowledge that you get when you’re working remote.

Chantal Roberts Yes, and especially in the US. I had obtained my Canadian licenses in a couple of provinces and I got special dispensation since I had been an adjuster for 20 plus years. One of the things that they have in Canada that we do not have in the United States is like that apprenticeship. You had to kind of serve under the master adjuster, much like you have an apprentice plumber and then you would have a master plumber, something like that effect. And I really actually like that idea a lot. But for the most part, adjusters are simply thrown in to the fire or the boiling water. Even though we have colleges, I think there are like 20 or so colleges, I might add. Don’t quote me on that. I might be right. Even though we have colleges that have a risk management and insurance major, they don’t teach claims handling it. If they do, it might be a week or a chapter. It’s definitely not a semester. How to handle claims. So that is absolutely not looked at in the broader scheme of. Insurance and insurance marketplaces.

Bill Sherman Well, and it’s interesting in terms of these are the things that you didn’t learn in your program or in your training, but you’re going to need, whether it’s relationship skills or being able to communicate because you are in a middle place, right? You’re between the people who have the claim and the people who want to minimize the payout on the claim. And some, if not all, are going to be disappointed on whatever number you pick. Right.

Chantal Roberts Okay. So I’m going to interject because I’m just like, he said minimize payout. And that is like such a big trigger point for me. Go for it. You know, because everybody does think that that is what adjusters do when in reality what we are supposed to be doing is paying the fair amount of the covered claim. Now, if we can get that done for $5 instead of $7, well then the insurance company is going to pay $5. It is no different than you go to the grocery store and seeing that apples are $5 a pound or you can get other apples for $7 about where everyone’s going to go for the $5 a pound apple kind of deals. That’s not any different. The insurance industry does not do a good job of educating their clientele. And adjusters are unfortunately that front facing people after someone has had a loss and they are in absolutely no mood to hear about their policy and about how they did not buy perhaps the right policy and so therefore how things are going to be covered or not going to be covered.

Bill Sherman So we could easily go on a tangent into history and even go into Lloyd’s and the original names and staking fortunes and basically writing a blank check back in the day. Right. And some of the names being wiped out. But I want to dive a little bit further on the first book and say, okay, we’ve identified the primary audience, which would be that rising middle level adjuster of the things you never really learned or nobody gave you the insight on. But you also had a secondary purpose of writing that first book for an audience. What was that?

Chantal Roberts That was to fill out some of my credentials. I am an expert witness or claims handling standards, practices and procedures, which is a really long title, which just basically means attorneys will hire me when the policyholder sues the insurance company to see if the insurance company handled the claim correctly. So I had already written several articles to fill out my CV and to make sure that I have this knowledge in this know how and that I can say, yes, I am an expert because I have published here, here and here. But I noticed that some of the opposing witnesses that I would be going up against would have written a book. So when the pandemic hit, all of the courthouses, of course, closed, which put the kibosh on my work because I could no longer do depositions or go to court or anything like that. And it was actually a perfect time for the insurance company and opposing counsel to settle the claim, which is great because nobody’s happy until the claim is is closed. Perfect. Fine. But that gave me the opportunity to write this book, The Art of Adjusting. So I could also have that little checkmark on my CV.

Bill Sherman And so you have the option in this case of crafting a topic for the book, which not only gives you the checkmark, but allows you to share some of the expertise that you have and things that you’re passionate about. Right?

Chantal Roberts Absolutely. Yeah, absolutely.

Bill Sherman So now let’s move to the second book where you say, okay, I’ve carved out a niche for myself in insurance adjusting. I’ve written to the mid-career adjuster. Who’s your next audience?

Chantal Roberts Actually, I had not considered this. I was just going to do one book just to check things off. And I know ironically, people are going to find this hard to believe, but there is not a big market out there for motor insurance books as potential listeners. It is shocking. I am very shocked, quite frankly. And so I am also very shocked that the Big five publishers did not beat down my door wanting to publish this. I just don’t understand why. But I had self-published because of course nobody is really interested in that. But because I. I like to say because I’m vain. I want to persist and stubborn. And all of these things. You know, some people say that’s bad. I say it’s good that I wanted to, you know, make sure I sounded intelligent because you can only read your stuff so many times. And so I deliberately hired an editor who didn’t know anything about insurance. And so I figured. I’m different for the first book. This is for the first book. Yes. The Art of Adjusting. And so I figured if she understood it, then definitely adjusters would understand it. And while she was editing The Art of Adjusting First book, she says, Do consumers know this? And I said, well, they should A, because their agent should be telling them this, and then B, they should. If the adjuster is doing what I’m telling them to do in this book. And she goes, I don’t I don’t think people know this. I didn’t know this until I read this book. And I’ve had several clients. You need to write a book for consumers. And so, boom, that that’s what I started to do right after I finished The Art of Adjusting.

Bill Sherman So you’ve finished this book and you’ve got a bit or the first book and you’ve got a challenge now. How do you write a book on insurance and insurance? Adjusting for a general audience that is probably not thinking it’s the greatest beach read ever.

Chantal Roberts Absolutely. Yeah. And I have to say it was difficult because I originally took the art of adjusting and was basically translating it into a consumer book, and I actually hated it. I myself and listen, I can talk about insurance for three hours straight. Just get me up on my soapbox. I will just start going after it. And if I knew if I hated this consumer book that was coming off as preachy and know it all and all of the bad things that you I mean, I wouldn’t read it. So hope that I say someone else would read it. And it occurred to me as I was teaching my risk management and insurance class in New York, even I teach it remotely. I live in Kansas. I teach it using The Incredibles, Pixar’s The Incredibles, the cartoon, because. I never could figure out how all the parts of insurance worked together until about ten years ago. Which is why I wrote the first book. So then I decided, well, I’m going to use one character or one family, one universe. And what these students all the way through the insurance sphere. And that is what gave me the idea, because students loved it, because they finally could relate these esoteric co-insurance, you know, and exceptions to the exclusions and all these big words that insurance companies use because we have attorneys writing our letters and our policies. They could understand what’s going on because they could see it happening and see how it would affect them. And that is what led to the second book, Once Upon a Claim Fairy Tales to Protect Your Assets. I started using fairy tales, nursery rhymes and fables to explain insurance concepts.

Bill Sherman No. Let’s go there. Give me an example of one of the fairy tales that you used to explain a concept. And in about 60s. Show us how you broke it down. What were you trying. Yeah, but what were you trying to teach? And what fairy tale did you use?

Chantal Roberts The one that I always mention and the one that everybody goes. Wow. I didn’t think about that is. Rapunzel and Goldilocks and the Three Bears. Both of these are put together in the book. And both of them are talking about a owner’s duty to a person who comes onto their property. In insurance, there’s three kinds of people who come in on your property. These two stories happen to talk about trespassers. The prince who goes up and down the tower to her puzzle is a trespasser. The Enchantress owns the property in Goldilocks. The bears on the property. She’s a trespasser. Now, if the prince falls down from the tower, then claws out his eyes because the enchantress has all these thorns and everything. Which is what happens in the grand weather. Grand version. She does not owe him a duty to keep that premises safe. Except not set out the trap because he’s trespassing. He’s an adult pose that he’s been there a couple of times. You should know better. Now, Goldilocks, on the other hand, is a child, and the Three Bears owe her a duty, just like they would a business invitee. Which means not only can they not set a trap, but they have to make it really safe for her because she’s a child and she doesn’t know any better, allegedly. So that is the difference. So I take the stories I tell them, and then I have a quote, moral of the story. And I break down these ideas of how these stories relate to insurance concepts.

Bill Sherman And you’ve written that in a way. That becomes accessible rather than heavy. Who do you want to pick up your book? At this point, who’s your ideal reader for this one?

Chantal Roberts I would love consumers to have this book because my original thought is. As you said, adjusters are only here to, you know, lessen the claims payment and yada, yada, yada. No, I explain what goes on. And I am honestly of the opinion that if we were all on the same page, if consumers knew the same things that adjusters knew. Like why we’re asking for things, why we asked things a couple of different times, yada yada, yada. Then you as a consumer, would be able to make your claim go faster. You would understand. You wouldn’t get upset. This being said, I know that this is a hard sell because as soon as I say the word insurance to anybody, they go, no. And they shut down and they won’t even go forward to the book.

Bill Sherman Right.

Chantal Roberts The book is hilarious. I mean, and I’m not saying that as the author. I mean, I would buy the book, but I would buy insurance books anyway because I’m a nerd, you know. But I also think that this would have a great audience with agents and the insurance companies themselves and hand it out to their clientele. Like, thanks for being a great customer, You know, thanks for buying your first house and getting insurance with us. Or, hey, you’ve got your first car. Here’s your book to tell you a little bit about your auto policy. I think that that would be a great warm fuzzy because right now the insurance industry is going through a hard market and we need to add value to our relationships.

Bill Sherman If you’re enjoying this episode of Leveraging Thought leadership, please make sure to subscribe. If you’d like to help spread the word about our podcast. Please leave a five-star review at ratethispodcast.com/ltl and share it with your friends. We’re available on Apple Podcasts and on all major listening apps as well as thought leadership leveraged.com/podcasts. Well and if I think about the insurance industry as a whole. It operates on asymmetries of knowledge. And it’s baked in. Right. Because, you know, almost from risk tables and actuarial tables in terms of what are the actual risks, what do we need to charge to be able to cover it? That’s the back end of the business.

Chantal Roberts Right. And nobody knows that.

Bill Sherman But then on the front side of the house, like you were saying, you get your policy. It’s in this little binder that good luck on, even if you’re a transactional attorney. Who understands contract law but doesn’t necessarily understand insurance law. It may as well be written in a foreign language. So you’ve bought a product that you don’t necessarily understand, and a lot of the marketing that has been done has really been done on, Hey, we’re easier to get a quote rather than here’s what you’re buying, right? So this knowledge asymmetry really sits at the heart of a problem and calls out for a thought leadership solution of the how do you educate people?

Chantal Roberts My gosh. You’re like preaching to the choir right now because I challenge my students each. And in fact, this Thursday, we’re going to be talking about marketing. And I’m making them watch some auto or some insurance commercials. And I’m asking them, what is every single one of them say? And every single one of them talks about price. And I challenge them to say. We are doing the wrong thing as insurance companies. We need to be educating our policyholders and I can educate a policyholder. Make it funny and do it in 30s. Or at least if I don’t educate, I will give them just enough knowledge to make them dangerous and to then go into saying like, Hey, I need to know more about this and go ask their agent. Because again, I don’t want these insureds not to be covered. I would love for them to be covered. And they just don’t know because they’re looking at perhaps they’re going perhaps they’re not talking to a human agent. Perhaps they’re talking to this robot agent that’s on screen and they just don’t know to ask. And the robot agent doesn’t sit. There are go, you’ve told me X, this makes me think of Y. Therefore, have you considered the possibility that you could have a loss of X? And you need insurance for it because the policy you just bought doesn’t give you insurance for it.

Bill Sherman And that leads to, like you said, when you advertise on price, you are weakening a relationship between the insured and the insurer. It becomes transactional. People are more likely to shop on price and move rather than have a relationship in an advisory relationship with an agent. And I mean, we can have a number of theories on whether you need just walk in capital coverage in certain cases. If there’s a state mandatory minimum for driver’s insurance, then you can say, give me the state mandatory minimums. But if you need any advising beyond that for anything else, then that’s a complex purchase. You want someone who understands.

Chantal Roberts I absolutely agree. I’ll give you an example. I think we have or I’ve handled let me put it this way. I have handled hurricane losses many, many, many hurricane losses. And I watched this newscast out of southern Texas where the reporter had interviewed a policyholder who had an estimate for $15,000 and they only got the policyholder. An insurance check or 3000. I mean, 15,000 was what would take to repair the building. Right. They got a check for 3000. And so there was this attorney they interviewed. An attorney is like, this is the insurance company, you know, lowballing and not paying the full amount. And then it added up. I actually reached out to that reporter and I said, look, there are so many things that could be the reason why you could have an actual cash value roof endorsement, meaning you’re only going to get paid actual cash value. You could have a windstorm deductible, which are usually like 5% of the total insured value, very high, which means, you know, maybe the insureds deductible was $10,000.

Bill Sherman Right.

Chantal Roberts And there are so many things. And we as the insurance companies don’t respond to these things and we should be responding to these things. So that would be a perfect example of how we can educate the public rather than letting this myth go on. Even in the news that we lowball, we pay us as little as possible. No, let’s educate people on what they have.

Bill Sherman And making the invisible visible visible.

Chantal Roberts Absolutely. I again, I think that and that’s another purpose of once upon a claim is if you knew what the adjuster was doing, if you knew what the adjuster was thinking then. Everybody would be happier. We could resolve the claim quicker, which is what the policyholder and the claimant third party claimant. That’s what they want to do as well. There are a lot of books like Don’t get me wrong, there are a lot of books out there because I was looking at them and their titles are something like, I’m going to share all the secrets of the insurance company to get more money. They’re written by attorneys and they promote that idea that the insurance company is the enemy. Where I’m different is I’m coming from a place like, look, the insurance company is not the enemy. I mean, sometimes as the policyholder or the claimant, you are just a lawyer. I’m not going to lie to you. We are all adults. Let’s all act like adults. Let’s have an adult conversation. Sometimes you’re wrong. Sometimes we are wrong. But if you knew what we were doing, you wouldn’t be so quick to judge or, you know, throw stones or however it might go.

Bill Sherman Well in a similar area winds up being medical billing, for example, where you get the bill in the mail and you can’t decipher it for love and money in the US. Right? Or other countries different experiences. But in the US you owe X and there’s been 3 to 10 different filters and people’s touching that be and all you know is you’ve got a statement of the due date. And at this point it just promotes frustration rather than an intelligent, educated consumer in conversation.

Chantal Roberts I will be the first to say I really dislike our health care, and the book is only property and casualty. It does talk homeowners auto and liability. I don’t I don’t talk health or life, but. Again, excellent example. My husband was seeking physical therapy on his knee and they told him at the reception desk, You won’t owe anything. Your deductible is paid, you know, blah, blah, blah. And we just got a bill for $350,000 or not. Sorry. $350. That’s a lot of money. $350.

Bill Sherman Well, that’s a whole lot of physical therapy, but yeah.

Chantal Roberts Yeah. And I for, for just to visit and we’re like, Whoa, whoa, whoa, whoa, whoa. Wait a minute. What happened here? And so I told him, you got to go push back. I mean, I could call them, but you’re not going to talk to me. I’m not you. So, yeah, I mean, it’s all confused as a health care person. You know, we all have our health care through our work, hopefully. And so we are insured, but we’re actually our employer’s insured. But we’ve never seen that insurance policy, so we have no idea what exclusion B one is. It. I hate that. I would really like to see the policy. Don’t tell me what B one is. Show me what b one is, and that’s what I’m telling adjustors to do. That’s what I’m instructing insureds to ask for so that they can see it and talk.

Bill Sherman So to pick up a thread of something that you mentioned earlier. Be in regards to once upon a claim your second up and you said, Wouldn’t it be useful if agents or insurance companies were handing this book out to either new customers or high value customers or young customers, whatever target segment you want to do? Right. You’ve been doing some proactive outreach on your own, and you’ve been planting seeds to sort of cultivate that idea. And you came up with an interesting approach to reaching out to agents and getting information. How are you? How are you planting that seed and getting the idea out there? Because I want to explore the work that you’ve been doing.

Chantal Roberts Yeah. So I actually obtained a small business loan to help me market this book Once Upon a Claim, and I found the Small Business Administration Small Business Development Center. Has a wealth of free information. And one of the things that my advisor told me is there is this database out there that basically lists every single company in the United States. You can go down by the codes that it uses that the government uses. You could go down by street addresses, by state, by county, whatever you wanted to do. And it spits out all of this data name of the owners or who the CEO is or who the marketing people are with their business name, their address, their email address, phone numbers, all of that kind of fun stuff, like how much they make in a year. This business with their credit rating is because you don’t maybe want to be going with people who don’t have good credit ratings. Who knows? Don’t know. Maybe you do. And those are the people that need the book. I have no idea. Anyway, I started downloading all of that and started sending these agents out postcards with a friend discount of 35% off the retail price and say hey go here and. And it gets them to a landing page which discusses why they should be handing this book out. So it’s a free resource. My library even has it so I don’t even have to go to the small business center. I get I log on from home virtually into my library because my library has it. It’s awesome.

Bill Sherman Well. And what I like here is in an age where whether you’re going traditional public publishing, hybrid or self, you’re looking saying what access to resources and databases do I have that already exist? Rather than having to go build your own network of insurance agents to do outreach. How can you leverage data that’s already been collected? To do a campaign.

Chantal Roberts Yeah. And I’ll tell you, I was actually really upset because the people who wanted to sell me these database lists, I, you know, it cost 300, 400, $500 to get, you know. But this is free. And the government has it for you. And I’m like, this is great. This is on taxes at work. Woo! And so I sent out 250 just to dip my toe in the water, and I have only gotten one back as a bad address. That’s how accurate the information is. I have actually bought. Mailing information before. Before I knew that this thing existed and I received dozens back and they and they go, I’ll guarantee that they’re 99% accurate and blah, blah, blah. Obviously they are not. I have received one back. So I think that’s.

Bill Sherman So that’s quality data going out. Now let’s ask the next question and explore what are you seeing in terms of response rate? Is it early to tell? I mean, you’re sending out postcards, so it might say lower touch signal. But what are you seeing on the campaign?

Chantal Roberts I, I actually chose postcards because I find that too many things go into spam. And I actually look at my spam because I want to make sure that I’m not, you know, missing something. But most people don’t. You know, like I said, my husband has thousands of spam emails. So I wanted a postcard because I wanted it to be something that agents actually looked at and physically touch and somebody touched. Yeah, exactly. So I haven’t seen any sales from it yet. But I don’t know if that’s because it is too soon to tell. Or maybe I’ve used too small of a sample size of 250. I did deliberately choose some states like California and Florida that are having a big insurance issues because of the hurricanes or the wildfires. But maybe. People again, even agents don’t quite grasp the idea. You know, like, why would I want to give away a book? Well, it could help you because people aren’t calling you going, What in the world is my adjustor doing? Or what am I paying you for? Or why are my premiums going up or anything like this? And I get that people won’t read this book. Front to back. It’s not that kind of book, but it might still be fun and entertaining.

Bill Sherman So let’s take a moment with the magic wand. It’s three years from now. Once upon a claim has been out and it’s been successful. My question is, what does success look like and how are you measuring it?

Chantal Roberts Wow, that’s a great question. I think, success. Would be. And I don’t know if we could measure it would be just to help people. You know, it stops this angst that goes on. And there are so many people in insurance. Hey, I there’s no way that you could ever say. You know, that is that is what the successful measurement is. The flippant answer, of course, is to sell enough books to repay the loan that I took out.

Bill Sherman Well, there’s multiple levels to success, right?

Chantal Roberts You know, So please, where the. But, you know, I mean, the real thing, the real goal is to help people. I just want to help people. And I’ve just got to get over that idea that this is about insurance and this is not going to be fun. I promise you. On fun. I promise.

Bill Sherman So on this journey, having written two very different books, one for a technical expert, one for a general audience. What’s a lesson that you can share about making that switch? Because you said, Hey, I was writing that book that I hated her version. She. How what advice can you share on making that audience switch and still working with the same content?

Chantal Roberts You mean for the authors?

Bill Sherman For the authors? Yeah.

Chantal Roberts Yeah. I would look into yourself and. And honestly, if you’re writing something, a passion project, even if it’s fiction, because now I’m working on a fiction book, That’s. That’s a passion. And if I did not like where it was going, I would have to change something. And that is essentially what I did with Once Upon a client. So I would say, listen to yourself. If you sit there and go, I would never read this. I hate this book that you were writing yourself. That’s when you need to take a step back and go, What would make me love it? Let’s do something really weird. And it’s not like I used all of the nursery rhymes. Like, I rewrote three blind mice to teach you how to read a policy. Some of them I keep very close to the way that they are. Row, row, row your boat pretty close. But I might add like 1 or 2 lines about flooding, for example. So and then in some instances, like I said, with the Rapunzel, I use the Brother Grimm version rather than the Disney version. But anyway.

Bill Sherman Brothers Grimm wind up having a little bit darker outcomes. So from an insurance perspective, I could see that the Grimm version would.

Chantal Roberts Work out.

Bill Sherman Well. Yeah.

Chantal Roberts Yeah. And then there’s the whole rhyming.

Bill Sherman Sort of on that.

Chantal Roberts Well, well, I was going to say then there’s a whole con about It’s the Grand Brothers annual. Yes, it is. His eyes get qualified burns and yada yada yada. So that’s my little dark in Shahid’s humor, which is why the book is fun. But anyway, I digress. But yeah, I would say as an author, to listen to yourself if you can’t see yourself reading this book, no one else is going to read that book.

Bill Sherman If you’re pushing yourself to write it and dreading writing it. Your audience is going to dread reading it or never read it. I think that’s great advice I get.

Chantal Roberts I’ll give you an example Right now with the new book that I’m writing, I can only write on the weekends and I relish it because I get down deep into the world that my main character lives in and I just love it. I don’t want to leave. I actually hate like when the weekend is over and I and I have to leave that world because I am just so fascinated by it. And that’s fun. So I hope that that would translate into my readers liking it.

Bill Sherman I think that signal of passion. Is a great one to end with in terms of thought leadership. Chantal, I want to thank you for joining today to talk to us about thought leadership, adjusting your assurance as one.

Bill Sherman Thank you for joining us.

Chantal Roberts Thank you for having me. Thanks. Bye bye.

Bill Sherman Okay. You’ve made it to the end of the episode, and that means you’re probably someone deeply interested in thought leadership. Want to learn even more? Here are three recommendations. First, check out the back catalog of our podcast episodes. There are a lot of great conversations with people at the top of their game, and thought leadership, as well as just starting out. Second, subscribe to our newsletter that talks about the business of thought leadership. And finally, feel free to reach out to me. My day job is helping people with big insights. Take them to scale through the practice of thought leadership. Maybe you’re looking for strategy, or maybe you want to polish up your ideas or even create new products and offerings. I’d love to chat with you. Thanks for listening.